One of the questions I’m asked more than almost any other is how I manage to fund my travels and have the time to do what I love at this stage of my life.

The answer is quite simple. I didn’t win the lottery, wasn’t born into money and didn’t inherit a fortune. I simply made a conscious decision, many years ago, to save heavily for my future, with pensions at the heart of that plan. I stuck to it throughout my career, increasing my contributions whenever I could afford to.

This isn’t financial advice, just my own experience. Everyone’s circumstances are different, but if sharing my journey helps even one person retire a little earlier and make the most of life, it’ll have been worth writing.

WHY I NEVER WANTED TO WORK UNTIL I DROPPED

I’ve never subscribed to the idea of working until I keel over. From a young age I remember hearing stories about people who died only a few years after retiring, and that always stayed with me.

Even in my early twenties, when a pensions adviser asked what age I wanted to retire, I didn’t hesitate. “Between 50 and 55.” That goal never changed.

During the final years of my career I really ramped things up with my contributory pension. At times I was routinely paying 30%, and occasionally more than 50%, of my gross salary into it. I also spent a lot of time learning how UK pensions and tax rules worked and made the most of every opportunity available. It meant tightening the belt at times, especially at the end of each financial year. I always believed the short-term sacrifice would be worth the long-term gain.

It certainly wasn’t all plain sailing. Two divorces took a sizeable chunk out of my pension; around half disappeared with the first and another quarter with the second. I don’t begrudge any of it, that’s simply part of the deal when you get married. If anything, it forced me to refocus, rebuild and stick even more firmly to my original plan.

If anyone thinks I’ve had life handed to me on a plate, you couldn’t be further from the truth. I grew up on a council estate in a working-class family, didn’t go to university and struggled at school. There were no trust funds, family wealth or inheritances waiting to bail me out.

I’ve been fortunate in many ways. I enjoyed a good career and, through my interest more than anything else, learned a huge amount about pensions as I went along.

So I thought I’d share a few things I’ve learned… well if I managed it, perhaps retiring early isn’t quite as out of reach as some people think.

THE MOMENT THAT CHANGED MY THINKING

A few years ago I found myself staring at a full moon, reflecting on life, the universe and all the wars and conflict going on around us. Viewed on a cosmic scale, so much of what absorbs our daily lives suddenly felt insignificant.

I had already reached my fifties and worked out that, if I lived to the average age for a man in the UK, I’d probably only get to see around another 140 full moons. That calculation even allowed for cloudy nights. Strange the things you think about, isn’t it?

Ever since then, whenever I see a full moon, I stop for a moment, look up and remind myself that my time is finite, don’t waste a minute! Plus, one day I’ll no longer have the energy to climb mountains, cycle across countries or happily rough it in hostels.

That realisation reinforced something I’d believed for years: if I could afford to retire early, I should. Experiences have a shelf life, and many are best enjoyed while you’re still fit and healthy enough to make the most of them.

Not long ago I came across a YouTube video that explains this far better than I ever could. I actually wrote this page long before I found it, but it’s the closest I’ve seen to capturing exactly how I feel about retirement, so I’ve added it and included a link below.

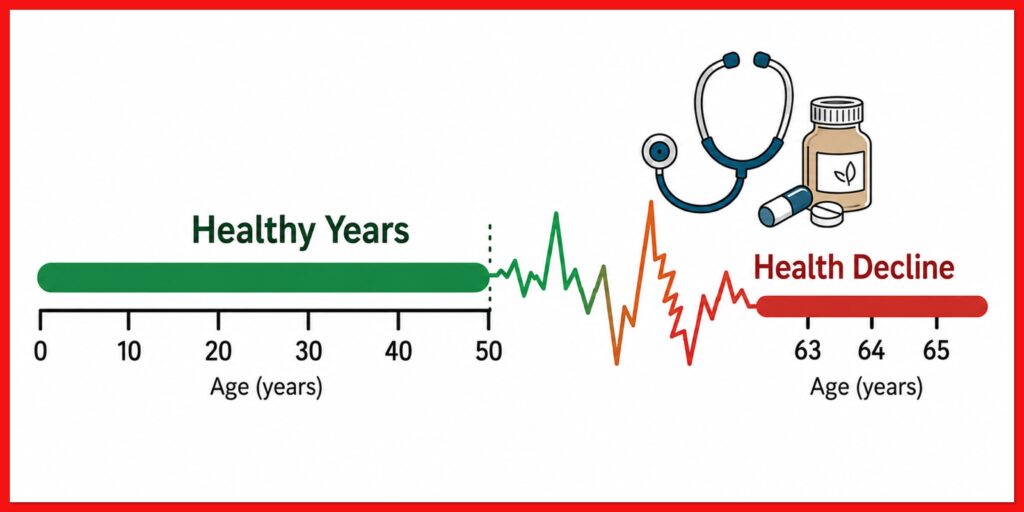

The statistic that struck me most was that the average healthy life expectancy in the UK is only around 63 years. That’s not our life expectancy; it’s the age at which, on average, our health starts to rapidly decline.

Of course, it’s only an average. Some people remain fit and active well into their eighties, while others become ill much younger. But the underlying message is difficult to ignore. If you can afford to retire earlier, you’re giving yourself more years in which you’re likely to be healthy enough to enjoy the things you’ve spent your working life dreaming about.

I’ve also included links to the Office for National Statistics data used in the video, together with a few graphs, so you can see the figures for yourself.

LINK TO VIDEO on this topic can be found below. It is really worth watching this IN FULL. If the pension pot values/numbers spoken about in the video appear unrealistically high, well, later on in this blog is a link to a second video that may appear a tad more realistic.

https://youtu.be/XzJZov7Ib4M?is=lnjXKLOnxFwk0csU

WHAT I’D DO DIFFERENTLY

If I could go back and give my younger self some advice, this would be it.

Start a pension as early as you can. Don’t put it off. The biggest advantage you have isn’t how much you invest, it’s time. Compound growth really is remarkable, and the earlier you start, the harder your money works for you.

Pay in more than the minimum. If your employer has enrolled you into a workplace pension, don’t just settle for the default contribution. Increase it whenever you can afford to. Pension contributions come out of your gross salary, so you benefit from tax relief and, depending on your circumstances that could be as much as 40%. It’s one of the few investments where the government effectively helps you along.

Have a target. Work out roughly how much you’ll need, then save with that figure in mind. That flashy new car or expensive holiday might be tempting, but I’d rather have bought myself years of freedom later in life. Looking back, I don’t regret making that choice for a second.

Stay the course. Life won’t always go to plan. Mine certainly didn’t. Divorce, unexpected bills and countless other things can knock you off track. Accept it, adjust and keep moving towards your goal.

Know when enough is enough. This is the one many people struggle with. Once you’ve reached the point where the numbers stack up, ask yourself whether another year or two at work is really worth giving up experiences you’ll never get back. It can feel like a leap of faith, but if you’ve done the maths and planned properly, trust it.

Get good advice. Choosing a financial adviser deserves the same effort, arguably more, than buying a house or a car. Shop around, ask questions and find someone you trust rather than simply accepting the first recommendation.

Plan to spend it – not pass it on. One subject that’s generated plenty of debate recently is the change to Inheritance Tax rules affecting pensions. Personally, I don’t think it should put anyone off saving into one.

Would I rather pensions weren’t subject to Inheritance Tax? Of course I would. That’s the selfish side of me talking.

But there’s another way of looking at it. The government has already given most of us generous tax relief while we’ve been building our pension, so it could be argued they’re simply clawing some of that back later. Perhaps that money could be better spent funding the NHS, education, national defence, the arts, emergency services, or fixing a few bloody potholes! Whether you agree with that or not is a matter of personal opinion.

Either way, it doesn’t change the purpose of a pension. For me, it’s there to provide an income in retirement, not to become a vehicle for passing wealth down through generations.

I certainly don’t intend leaving too much of mine behind.

THE BIG QUESTION… HOW MUCH IS ENOUGH?

For me, this was the hardest part of retirement planning.

Staying in work would almost certainly have increased my pension pot and ‘perhaps’ given me greater financial security, but it would also have cost me something far more valuable: time.

So, in 2021, aged 56, I finally sat down and did the maths.

Like most people considering retirement, the biggest question wasn’t how much money I had, but how much I’d actually need for the rest of my life. This is directly liked to the type of person I wanted to be, frugal, savvy or extravagant, spending habits and style will massively alter the answer to this question,

I worked out my monthly spending, separating essentials from the lifestyle I wanted to enjoy. Then I factored in inflation, tax, my mortgage, household bills, investments, State Pension entitlement, expected pension growth and, perhaps most importantly, my own appetite for risk.

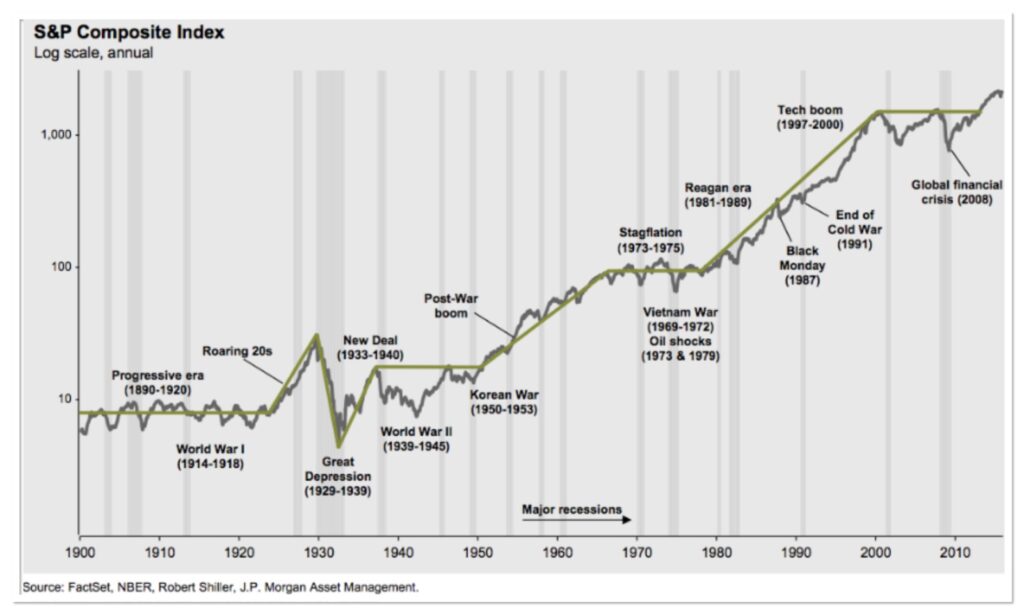

None of it is an exact science. You’re making educated assumptions about the future, because nobody, not even the best financial adviser, can tell you exactly what markets will do over the next thirty years.

That’s why it’s important not to obsess over short-term market movements. There will always be peaks and troughs. History tells us that markets recover, although nobody can guarantee how long that will take. The trick is not to panic every time there’s a downturn.

One thing that gave me peace of mind was keeping a separate emergency fund in cash (in a high interest or other account not linked to stocks and shares). Ideally, enough to cover around six to twelve months’ living costs. That way, if markets fall sharply, you can draw on your savings instead of selling pension investments at the worst possible time.

Modern drawdown pensions are incredibly flexible. My own preference has been to take twelve equal monthly payments, treating it like a salary. It suits me, keeps my finances predictable and allows the rest of my pension to remain invested.

Finally, don’t underestimate the value of simply being content with what you have.

It’s easy to compare yourself with people who seem wealthier, but there’s always someone with a bigger pension, a nicer house or a newer car. At some point, you have to decide what’s “enough” for you.

For me, enough meant having the freedom to spend my time doing the things I love while I’m still able to do them.

I’ve included another excellent video below which looks at exactly this question. Like the first one, the narration won’t win any awards, but don’t let that put you off, the content is well worth your time. https://youtu.be/AFK744Ba5vo?is=fGqIMF3q1r8-Aq5y

It may just help to reframe your thinking.

TESTING THE WATER

Walking away from my main career wasn’t quite as simple as handing in my notice and disappearing into the sunset.

I briefly considered consultancy or part-time work in my old profession, but both would have tied me down more than I wanted. I was looking for flexibility, not another career.

So I did something completely different and got myself an HGV licence.

I’ve always enjoyed driving, so the idea of spending time out on the road appealed to me. Looking back, it turned out to be one of the best decisions I made.

At the time I was still a little nervous about whether my pension would last, I was looking purely at the numbers and factoring-in all kinds of unnecessary permutations and risks. But, knowing what I now know, I needn’t have worried. But on the plus side, driving trucks gave me the confidence to ease myself into retirement rather than jumping in at the deep end. There was another important reason too. Emma wasn’t ready to retire at that point, so working part-time felt like the right balance for both of us.

For the next few years I worked around eight to ten days each month. It covered the cost of the odd trip, delayed the point at which I needed to start drawing my pension and, perhaps most importantly, confirmed that I’d made the right decision.

It also meant I always had another skill to fall back on if I ever needed it.

Working on a zero-hours contract suited me perfectly because, for once, I was the one calling the shots. I could decide when I wanted to work, how often I wanted to work and, if I fancied disappearing off travelling for a few weeks, I simply didn’t book any shifts.

That said, I’m not a huge fan of the gig economy in general.

Too often employers expect complete flexibility from their workforce without offering much in return. Many workers simply can’t afford to turn work down or insist on conditions that suit them.

I was fortunate. I was in a position where I could dictate the terms, which made it work brilliantly for me. I appreciate that isn’t the reality for many people, and I still think we’ve seen employment protections move in the wrong direction over recent years.

For me, though, it was the perfect stepping stone between full-time work and full retirement.

LOOKING BACK

If I could rewind the clock, I’d probably contribute even more to my pension from the very beginning, even knowing what my two divorces would eventually cost me.

Without question, my pension has been the single most valuable financial tool I’ve ever had. It frustrates me that so many people seem to overlook what’s on offer, often because nobody has ever properly explained it to them.

Personally, I’d like to see far more emphasis placed on pensions and retirement planning in schools, workplaces and by government. Most people spend decades earning money, yet very few are taught how to make that money work for them later in life.

I owe a lot to my dad. He left school at fifteen, started work on the London docks, later became a council worker and eventually joined the Fire Service. Through a combination of hard work and good fortune, he also managed to retire early. However, he had an old-style Defined Benefit (DB) type of pension rather than the Defined Contribution (DC) one that I have. The latter is more common these days, and there are pros and cons to each.

Watching him made me realise that retiring before old age wasn’t just something wealthy people did. It was something ordinary people could achieve if they planned carefully enough.

My own journey has been very different, but the lesson was the same.

If this page encourages even one person to take pensions a little more seriously, increase their contributions or simply start planning earlier, then writing it will have been worthwhile.

As for me, if I’m still around in twenty years’ time and still travelling, I’ll happily come back and let you know whether the plan worked.

So far, so good.

Happy travels.

HINTS AND TIPS

Most of my travel blogs finish with practical information, so it seems only right to do the same here.

When I decided to retire, I spent a long time researching financial advisers before choosing one. I wasn’t looking for the cheapest; I wanted someone I trusted, who explained things clearly and whose approach suited me.

I eventually chose Guy Stout, a Chartered Financial Planner at Doyle & Palmer, and I’ve been very happy with the advice I’ve received.

Emma uses a different adviser, Sally Read-Cayton at Foster Denovo, and has had an equally positive experience.

As always, I’m not recommending that you use either of them simply because I do. Just as I don’t receive commission from the travel links on this blog, I don’t receive anything for mentioning them here.

My advice is exactly the same as when choosing almost anything important in life: do your homework, speak to several advisers, compare fees, ask plenty of questions and go with the one you trust the most. Even seemingly small differences in annual fees can make a significant difference over the lifetime of a pension.

Finally, be careful. Pension scams are sadly all too common. Always check that any adviser is authorised by the Financial Conduct Authority, verify their contact details independently and carry out the usual checks before committing your money. Link to FCA website

It’s been a tough (but enjoyable) paper-round.